Mobile operators’ SMS revenues may be under pressure from mobile messaging apps such as WhatsApp, iMessage and others. The only real issue is where, when and how much over the top apps will reduce mobile service provider revenue.

To be sure, Informa Telecoms & Media still forecasts that mobile operators will still generate a total of $722.7 billion in revenues from text messaging revenues between 2011 and 2016.

Third-party providers of over the top (OTT) messaging services will earn about $8.7 billion in 2016. That disparity in revenue illustrates the issue.

The big problem is not that OTT providers take so much revenue from mobile service providers, so much as OTT messaging essentially destroys the existing business, rather than shifting share to new contestants.

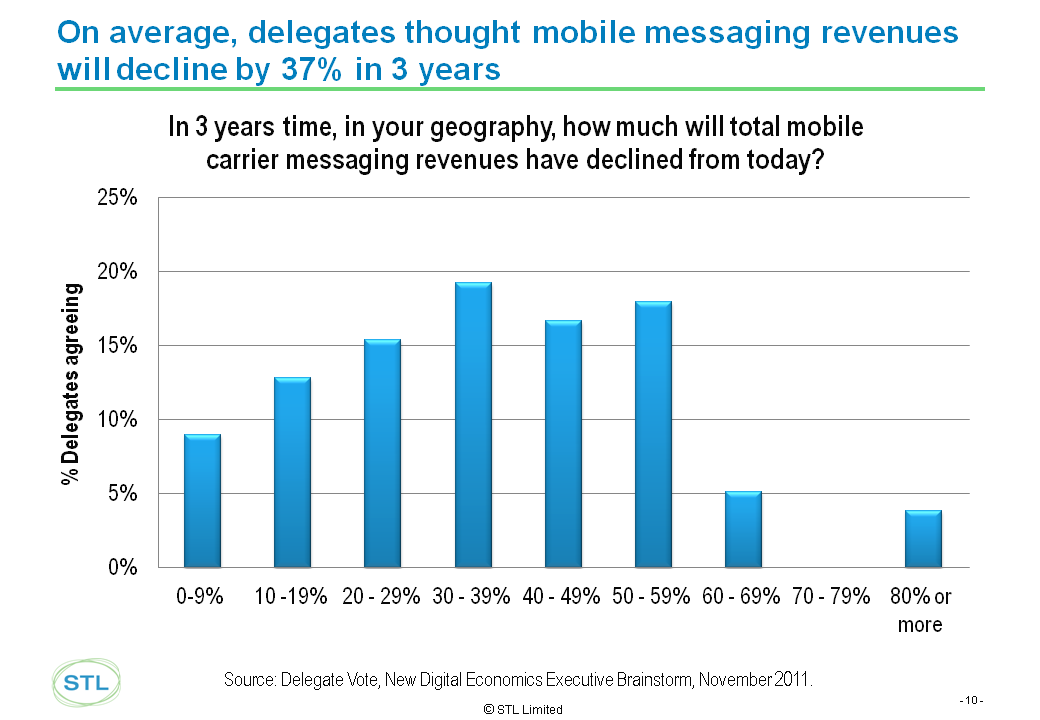

Text messaging revenue could decline 40 percent over the next three or four years in the European and Middle East markets, many executives predict. About 84 percent of respondents to a Telco 2.0 survey thought the main reason for such declines was the expected price reductions mobile service providers would adopt to compete with OTT services and apps.

In many ways, that is precisely what service providers have encountered when facing over the top voice apps. The OTT providers do not so much take revenue away from incumbent service providers as destroy the market.

Informa Telecoms & Media estimates that every 10 percentage points increase in smart phone penetration could cost Western European operators $1.19 billion in voice and messaging revenues and $306 million for their Eastern European counterparts.

In 2010, for example, mobile operators made on average only $13.21 per user per year from mobile VoIP services.

In other words, VoIP turns out not to be such a great product for incumbent service providers.

In fact, some might argue there is almost no way incumbent service providers can avoid losing both voice and messaging revenue to over-the-top applications, no matter what they do.

Mobile service providers lost an estimated $13.9 billion in text messaging revenue in 2011, as subscribers turned to outside social messaging apps, according to researcher Ovum.

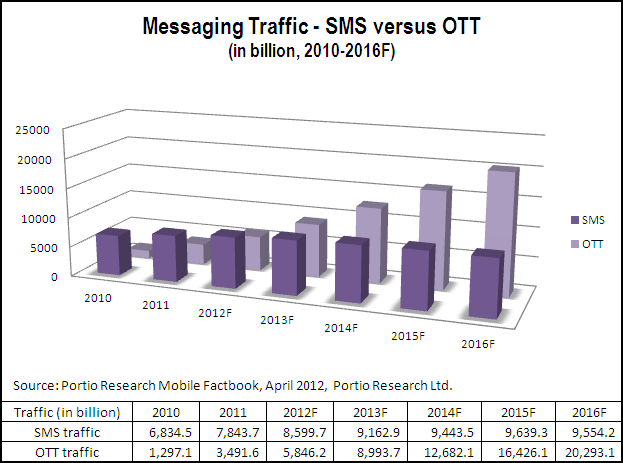

Globally, Informa forecasts that SMS traffic will total 9.4 trillion messages by 2016, up from 5.9 trillion messages in 2011. However, SMS’s share of global mobile messaging traffic will fall from 64.1 percent in 2011, to 42.1 percent in 2016. Traffic is not revenue, though.

At the same time, global mobile instant messaging traffic will increase from 1.6 trillion messages in 2011 to 7.7 trillion messages in 2016, doubling its share of global messaging traffic from 17.1 percent in 2011 to 34.6 percent in 2016.

“There will not be a uniform decline in mobile operators’ SMS traffic and revenues as a result of the adoption and use of over-the-top messaging services,” says Pamela Clark-Dickson, senior analyst, Mobile Content and Applications, at Informa.

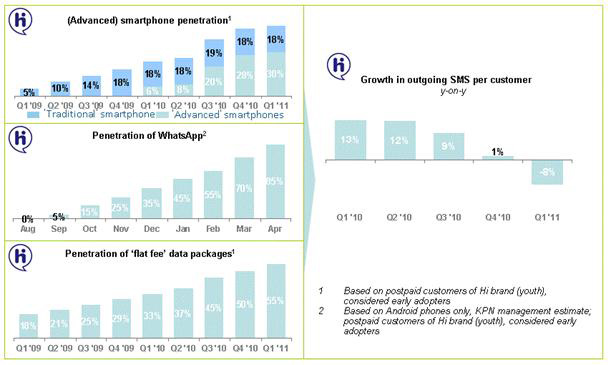

Text messaging traffic on the KPN Netherlands network shows the impact of changing use of text messaging and OTT apps. SMS traffic has been declining since the third quarter of 2010, it appears, after hitting a plateau in early 2010.

While Informa is forecasting either slowing growth or even a small decline in person-to-person SMS revenues in some developed regions and countries, total global SMS revenues will increase at a compound annual growth rate of three percent over the next five years.

Western Europe will generate the highest amount of SMS revenues globally between 2011 and 2016, totalling $174.1 billion, followed by Asia Pacific Developing, where SMS revenues will total $173.8 billion between 2011 and 2016.

.jpg)