Strategists in urban and other relatively-dense areas in developed markets typically do not worry excessively about wide area backhaul services. That generally is not the case for ISPs or mobile service providers working in rural and thinly-populated areas.

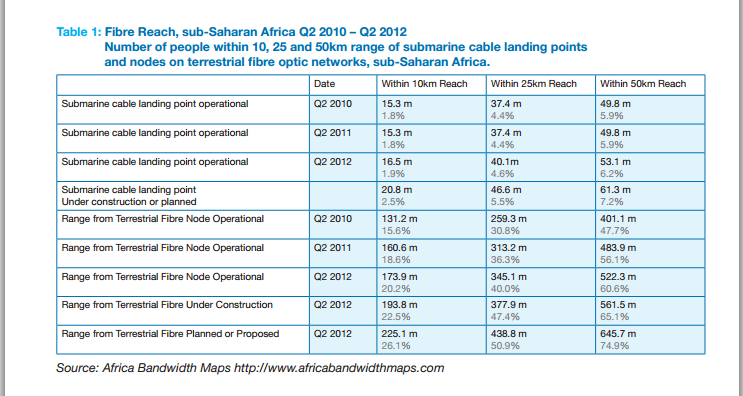

In June 2012, some 341 million people in sub-Saharan Africa lived beyond a 50-kilometer range of a terrestrial fiber optic backhaul network. What that could mean is a huge need for middle-mile connectivity provided by wireless networks, one might argue, since 50 km is a feasible distance for some microwave systems, assuming terrain is favorable.

The average price of a broadband connection represents just 1.5 percent of monthly income in Europe, but can represent over 100 percent to several thousand percent of monthly income for some African countries.

This level of affordability varies tremendously across sub-Saharan Africa, with the cost

of broadband access ranging from 5.7 percent of Gross National Income (GNI) per capita in South Africa, to 59.9 percent in Kenya, 259 percent in Madagascar, 1,070.8 percent in Ethiopia and 2,595 percent in Guinea Conakry, according to the International Telecommunications Union.

And there is no question but that new sources of wide area Internet access are having an impact on costs. In those countries recently connected to submarine cables, broadband has become much more affordable and the growth in broadband subscribers has accelerated.

Following the entry into service of the SEACOM and EASSy submarine cables in Kenya, for example, the price of fixed broadband decreased from 261 percent of GNI per capita in 2008 to 60 percent in 2010, in Mozambique from 312 percent in 2008 to 60 percent in 2010, and in Tanzania from 174 percent in 2008 to 50 percent in 2010.

These include Uganda (through Kenya) where the price of fixed broadband decreased from 375 percent of GNI per capita in 2008 to 36 percent in 2010, Ethiopia (via Sudan and Djibouti) from 2,721 percent in 2008 to 1,071 percent in 2010, and Burkina Faso (through Senegal, Cote d’Ivoire, and Benin) which decreased from 4,466 percent of GNI per capita in 2008 to 194 percent in 2010.

In Guinea Conakry, one of the eight countries that is wholly dependent on satellites, the monthly price of fixed broadband usage has decreased slightly to 2,595 percent of

GNI per capita in 2010 compared to 2,824 percent in 2008.

Growing availability of optical connections has reduced, but hardly eliminated, the need for satellite backhaul.

The supply of international trunk Internet bandwidth supplied by satellite to the sub-Saharan region reached a peak of around 9 Gbps in 2008, but has dropped back since then.

Kenya, for example, peaked at about 2 Gbps of international bandwidth supplied entirely by satellite in July 2009 until the entry of the SEACOM (2009), followed by the TEAMS (2009), EASSy (2010) and LION2 (2012) submarine cables.

That has dramatically increased the supply and decreased the cost of international bandwidth. Within two and half years, Kenya’s international bandwidth had increased from 2 Gbps to 53 Gbps by December 2011, but the amount supplied by satellite had shrunk to 108 Mbps, according to the Commonwealth Telecommunications Organization.

In June 2012, eight African countries remained 100 percent dependent on satellite for their international connectivity. Even in those countries with national fiber backbones, another 298 million or so people lived beyond the reach of terrestrial fiber networks, according to the Commonwealth Telecommunications Organization.

Most of Africa’s main urban hubs are now reached by fiber transmission backbones connected to submarine cable landing points, however.

In June 2012 a total of 40.1 million people lived within a 25 km range of a submarine cable landing point, but 345.1 million people lived within a 25 km range of a terrestrial fiber optic node.

By the time new networks enter service in 2013 to 2014, about 377.9 million people will live with a 25 kilometer range of an optical access point. Over the next three to five years, that range will increase to 438.8 million.

That still will leave 423.2 million people, or 49.1 percent of the population, beyond a 25-km reach of a terrestrial fiber optic node.

No comments:

Post a Comment