There are any number of reasons why regulators prefer that the U.S. mobile market continue to feature four national contestants, instead of the three that would remain if Sprint an T-Mobile US were to merge.

There are any number of reasons why regulators prefer that the U.S. mobile market continue to feature four national contestants, instead of the three that would remain if Sprint an T-Mobile US were to merge.

The issue is whether that is possible, long term, irrespective of what regulators might prefer.

Sprint, though growing revenue, continues to show an operating loss, and has since at least 2006. T-Mobile has been on a subscriber upswing since the start of 2013, but profits and net income are the issue.

T-Mobile US net income dropped by nearly 90 percent in 2013, for example, the direct result of a successful subscriber market share attack.

Total T-Mobile US revenue in fourth quarter 2013 rose 10.2 percent after taking into account the acquisition of MetroPCS.

But branded postpaid average revenue per user fell by 2.9 percent. Cost per new customer rose by $10 during the quarter to $317.

As a result, T-Mobile US's fourth-quarter cash flow (leaving out non-recurring items) dropped 7.8 percent from the third quarter of 2013.

In 2012, T-Mobile US posted operating margins of 9.6 percent; this figure shrank to 4.1 percent in 2013.

Debt burdens also are rising. T-Mobile US has announced capital spending plans of $4.3 billion to $4.6 billion in cash, compared to projections of cash flow before cash interest and taxes of $5.7 billion to $6 billion.

The point is that a continued marketing war will hit earnings at potentially all the four national carriers, but will eventually harm Sprint and T-Mobile US even more, as those two carriers do not have the financial strength of AT&T and Verizon.

Already weak, compared to AT&T and Verizon, Sprint and T-Mobile US would eventually be weakened further by a prolonged marketing war.

Such numbers are the reason some might argue that long term competition in the U.S. mobile market would be strengthened were Sprint to buy T-Mobile US.

The combined company would have more than 50 million postpaid subscribers, much closer to Verizon Communications' 95 million and AT&T's 70 million-plus postpaid customers.

Some might argue that since none of T-Mobile US customers are on contract, they are susceptible to churn.

That only reinforces the point: as feisty as T-Mobile US is, and Sprint might become, both service providers are dangerously smaller than AT&T and Verizon, a fact that would be critical if a price war saps revenues at all four carriers.

The point is that, one way or the other, the U.S. mobile market is likely to consolidate further, no matter what the Federal Communications Commission and Department of Justice might prefer.

But that market-driven contraction will come when both Sprint and T-Mobile US are even weaker than they are at present.

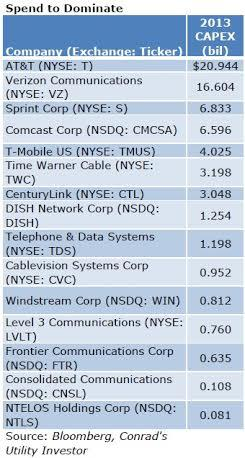

Capital budgets are just one example of the disparity.

No comments:

Post a Comment