|

| source: ABI Research |

The next step likely will involve market consolidation between mobile provider Bouygues, which had lost its bid to acquire SFR itself, and Illiad, owner of Free Mobile, the low-cost mobile service provider which has been attacking the French mobile market with low-price offers.

The French market rearrangement also suggests some differences from the drivers of U.S. communications market consolidation.

Consolidation in the U.S.cable TV and telecom industries has occurred on separate tracks: up to this point the key mergers have been intra-industry rather than inter-industry.

That suggests revenue growth strategies have largely been viewed as a matter of amassing additional scale within each industry--cable TV and telco--without a fundamental requirement for trans-industry positioning.

Verizon and AT&T have pinned their hopes largely on continued growth of their mobile businesses, even though both own significant fixed network assets. Likewise, cable operators have seen subscriber growth primarily as a matter of gaining more scale within the cable TV business.

|

| source: Venturebeat |

In Western Europe, mobile service providers indicate by their acquisitions that revenue growth likely cannot come from the mobile segment alone, though scale helps.

And Altice sees additional revenue growth for itself as coming primarily from cross-industry acquisitions.

In large part, that is a result of Altice’s large cable TV market share, which offers little remaining out of territory gains, as well as an emphasis on quadruple-play offers expected to drive revenue growth.

The other issue is that aggregate telecommunications revenue has been dropping in Western Europe for some years.

Because of that trend, the “grow from mobile” strategy, which continues to underpin AT&T and Verizon strategies, is viewed as untenable in Western Europe.

Instead, growth is seen as coming from quadruple-play offers that combine mobile with fixed network triple-play services. That, in turn, is a way of acknowledging that each contestant will have a harder time growing by adding subscribers, and instead must sell a wider range of products to a smaller or slowly-growing number of subscribers.

Many observers think Bouyges still has to make a key acquisition, as it now finds itself roughly in the position of Sprint in the U.S. mobile market, trailing the top-two providers by some distance.

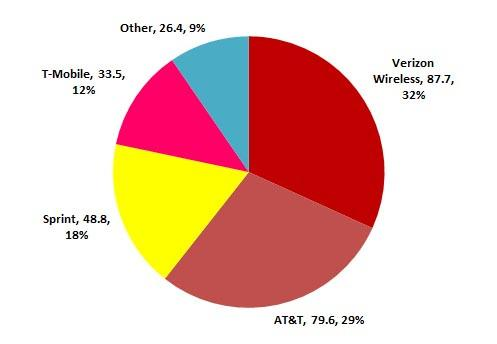

Verizon Wireless has about 32 percent of U.S. mobile subscribers, while AT&T Mobility has about 29 percent share. Sprint has about 18 percent subscriber share, while T-Mobile US has about 12 percent share.

Share of revenue and profits is another matter. Sprint and T-Mobile US are losing money, while only Verizon Wireless and AT&T Mobility actually are profitable.

And most of the revenue earned in the market is earned by AT&T Mobility and Verizon Wireless.

Verizon earns about 38 percent of U.S. mobile service provider revenue. AT&T gets about 34 percent of revenue.

Sprint gets about 17 percent of revenue, while T-Mobile US generates about 11 percent of revenue.

The point is that Bouyges, Sprint and T-Mobile US all face similar challenges: they are far behind in market share, in markets where scale matters, long term.

But Bouyges will face some of the same regulatory issues it would have faced had its bid for SFR been accepted.

That deal would have vaulted Bouyges into first place for French mobile market share, but also likely would have engendered opposition from French regulators, who continue to desire a minimum of four service providers in the market.

Any combination of Bouyges and Illiad would raise the same issue, but only at a lower level of market share held by the new company.

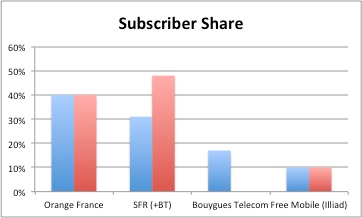

Orange (France Telecom) has about 40 percent share of the mobile market. Numericable now has 30 percent market share. Bouyges has about 17 percent share, while Illiad has about 10 percent share.

Combined, Bouyges and Illiad would have about 27 percent market share.

|

| source: Gigaom |

Sprint and T-Mobile US face a similar issue in the U.S. mobile market, as U.S. regulators likewise prefer a mobile market lead by four major national suppliers, and oppose a reduction to three leading providers.

No comments:

Post a Comment