Quite often, spending ramps up when a next-generation network platform is being deployed, when competition heats up or a major new revenue source requires such investment.

Spending often ramps down when a network build is finished, when a major recession or other financial disturbance pinches revenues or when service providers decide to momentarily shift resources elsewhere (acquisitions; major spectrum purchases or required investment elsewhere in the business).

Sprint and AT&T offer examples.

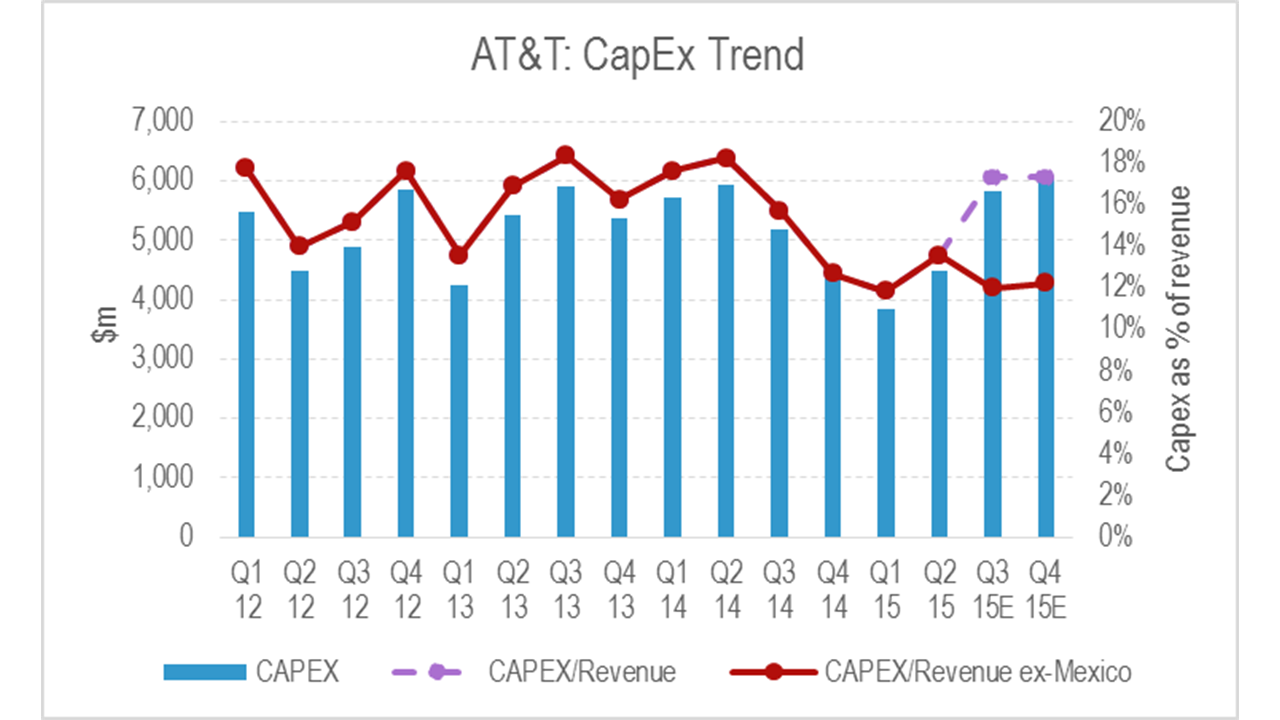

AT&T plans on significantly lower capital investment over the next few years. In some part, that is because AT&T has finished its fourth generation network build, is deploying capital to make acquisitions, and likely is conserving on capital for expected spectrum auction investments as well.

From the second quarter of 2013 to the end of the second quarter of 2014, AT&T spent on average $5.7 billion a quarter on network-related infrastructure.

Since then, the average is $4.4 billion (excluding capital related to AT&T Mexico networks investment), representing a dip in U.S. capex of perhaps 21 percent. But some might argue that capex dipped for a year between 2014 and 2015 before resuming a typical profile.

Some might argue AT&T capex has not shrunk, but it has shifted to new locations outside the United States.

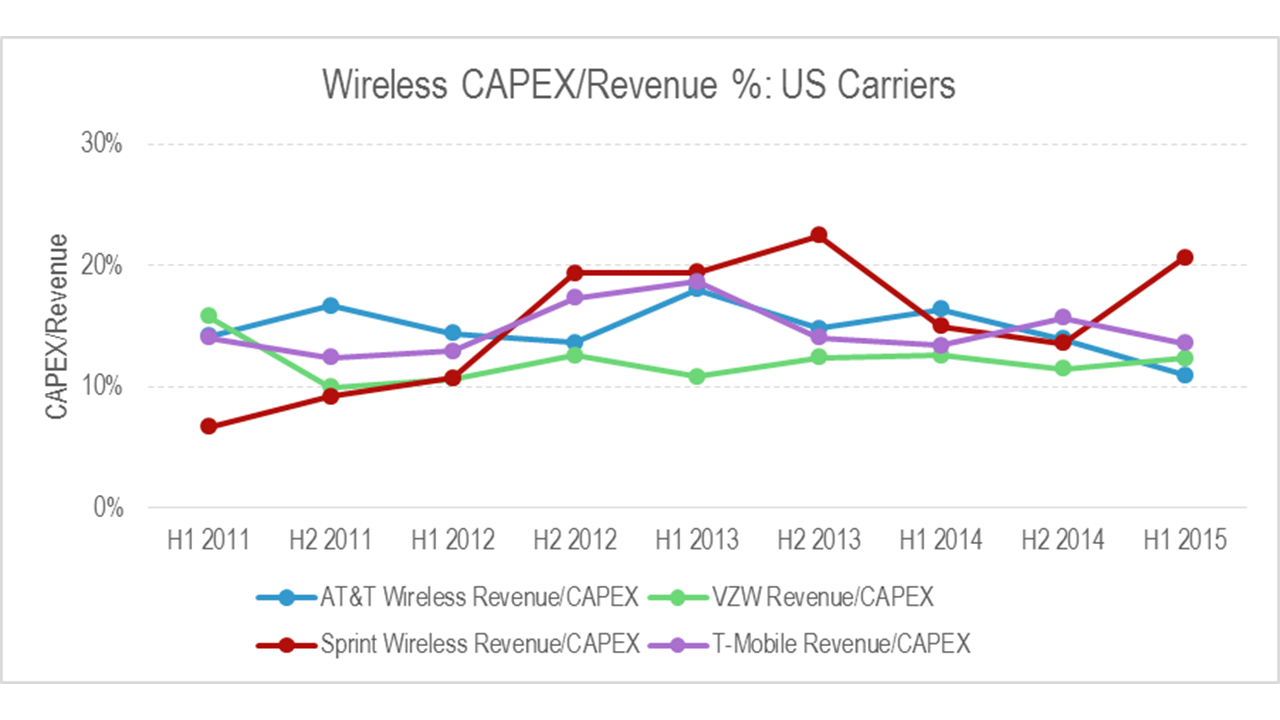

Sprint, on the other hand, after a similar slowdown in 2014, has hiked capex--as a percentage of revenue--to remedy network deficiencies, compared to other leading competitors. The key there is “revenue.” Sprint simply has less revenue available to offset any incremental move in capital spending.

On an aggregate industry-wide basis, U.S. mobile carriers have grown capex since about 2012. Given expected spending on additional spectrum--and new expected competitive threats--overall capex might remain at higher levels for some period of time.

As much as a rational mobile service provider executive might prefer to spend a lower percentage of revenue on capex, or even lower gross amounts, the market might continue to require relatively higher levels of investment.

The entry of Google Fi and the coming entry of Comcast into the mobile business are examples of how competition could change in the future, irrespective of any continuing market share battles between the four big national service providers.

No comments:

Post a Comment