In other words, access is necessary, but “who” supplies the access, and what the business models are, can change. That question matters greatly for traditional fixed telecom network services providers, mobile service providers, cable TV companies, independent Internet service providers, satellite and fixed wireless ISPs and government-related or non-profit ISPs alike.

One fact seems clear enough: U.S. mobile revenue will drive growth in the U.S. communications business in 2016, offsetting declines in the fixed network segment.

The important fact of note there is revenue contraction in the fixed network segment. The possibly more important fact is the emergence of new competitors, ranging from Google Fiber to independent ISPs offering gigabit services, plus municipal ISPs.

Another key trend: perhaps municipalities are learning to focus on providing incentives for ISP investment, rather than focusing on revenue to be directly gained in the form of fees on such efforts.

In that sense, what happens in terms of local government policy could have as much impact on ISP investment and gigabit network deployment as anything done by the Federal Communications Commission at the national level. In fact, some would argue the FCC has actually made investment decisions more difficult for most mobile and fixed operators.

On the other hand, such limits make more feasible new competition by firms with different cost structures and revenue models. Some might make the argument that the long-term effect will include the imposition of usage caps by many of the largest ISPs, as more-difficult business models will place a premium on controlling costs.

“Unlimited usage” arguably is among the potential cost elements that have to be adjusted.

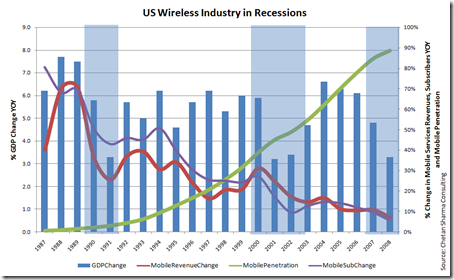

During periods of U.S. economic growth or recession, the mobile industry has faced a generally-declining rate of revenue growth, from 1987 to the present.

Taking into account the different accounting treatment of device sales and recurring revenue, U.S. mobile service provider revenue has been nearly completely unaffected by the substitution of device installment plans, compared to the previous bundled approach, where discounted phones were amortized over the life of a service contract.

That could change.

If a shift to device leasing affects business models more than a shift to installment plans, one can expect a focus on operating costs will come rather rapidly.

The point is that the Internet access business could change significantly, in terms of supplier base. Incumbent telcos likely will have a smaller share of the fixed market, and eventually less share in mobile as well, as new providers take more share.

No comments:

Post a Comment