It has generally been argued that big telcos are not good at “innovation.” It is less often said that companies are similarly situated, but an argument can be made that this also is true. Such assertions are hard to test.

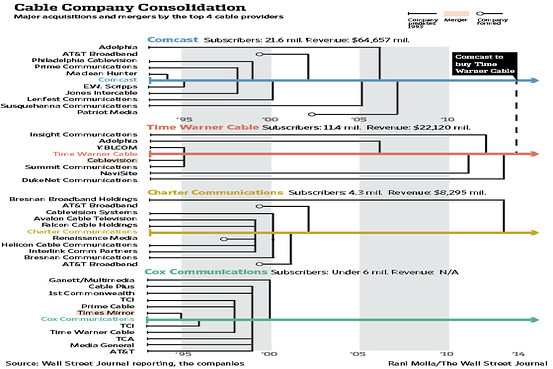

The reason is simply that many big telcos and cable TV companies literally have grown by acquisition, not by organic growth. In other words, by design, it has proven impossible, as a practical matter, to test “how good” telcos or cable TV companies might be at innovation as a driver of revenue growth.

In the U.S. market, for example, the largest suppliers--AT&T, Verizon, Comcast and Charter--all have grown principally by acquisition. In other words, it is impossible to determine how good they might have been, had a different, organic growth path been chosen.

It therefore never has been a core or essential strategy to “get good at innovation.” It has been a core strategy to “get good at making acquisitions.”

That makes rather easy a prediction that future growth for these tier-one suppliers will continue to be lead by acquisition, not organic growth. Size alone makes that imperative. Big companies generally cannot grow fast enough strictly by “organic” means, and all the biggest U.S. communications and media firms have annual revenue between $60 billion and $160 billion. Charter Communications is the latest member of the “$60 billion or more annual revenues” ranks, based on its acquisitions of Time Warner Cable and Bright House Networks.

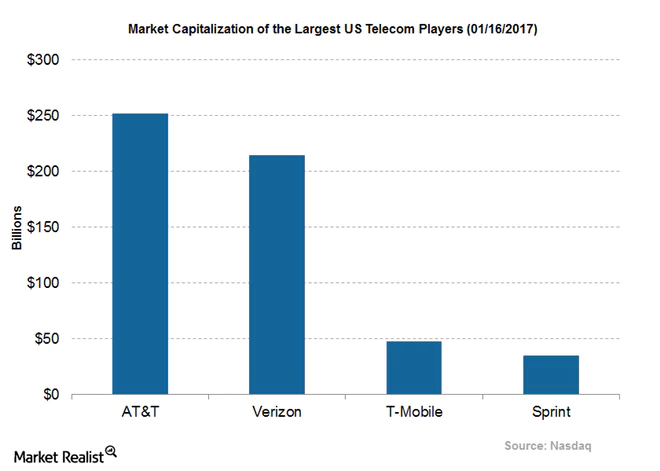

One might well argue that the reason Sprint and T-Mobile US are strategic sellers, not buyers, is size alone. Neither of those firms has the aggregate revenue mass to match up with AT&T, Verizon, Comcast or Charter.

Nor, given the size of the biggest firms, will small acquisitions matter much. Moving the revenue needle just 10 percent means grabbing assets adding between $6 billion and $16 billion worth of revenue annually.

That is why, as important as incremental and tactical operations might be, the path forward, for the biggest U.S. firms, relies on growth by acquisition. The only issue is what directions those moves will take.

It also matters how antitrust authorities choose to define the relevant markets that stand to be reorganized. Even if executives behave in ways that suggest how they see their markets and customers (mobile execs pay close attention to other mobile competitors; cable and telco fixed network execs pay most attention to each other; video providers pay most attention to other video suppliers), major changes might well require a redefinition of “markets and competitors,” or else horizontal combinations will not be possible.

Vertical combinations likely will fare much better, as approval will not require bending of traditional antitrust metrics.

The bigger point is that it is possible to argue that telcos and cable TV companies never have been that good at innovation, but that it doesn't matter. They have grown by acquisition. And that is what they need to be good at.

{kind=link}

No comments:

Post a Comment