Generally speaking, as much as service provider executives talk about "moving up the stack" to avoid becoming a "dumb pipe," there is justifiable skepticism about whether that is possible, in many settings. History suggests it is hard to do, hard to do well, and almost never has resulted in significant revenue upside.

There are a few salient exceptions--mobile banking in some markets and video entertainment services in a growing number of markets.

But much depends on where a particular actor sits in the value chain, and what part of the industry that actor occupies.

If the core business is undersea capacity, it is easy to see why skepticism about such moves up the stack is worth attempting. When the core business is "pipe," moves "up the stack" are unlikely to be easy, and might actually be dangerous, as it is so far outside the core competence of the providers.

On the other hand, such efforts already have proven most successful for retail suppliers of communications services who historically come from the "applications" part of the business, and for whom "dumb pipe" has become a reality only in the internet era.

The best example is internet access service. That is the classic dumb pipe service. Traditional voice, messaging, specialized enterprise and business data networks, paging and video services were applications, where the network exists only to support delivery and use of the apps.

“Moving up the stack” might be among the most-difficult challenges a service provider ever faces. Arguably few such attempts ever have succeeded on a massive or even significant scale, where it comes to increasing revenue contribution.

And yet it is hard to argue that the effort must be undertaken. The reason service providers want to move up the stack is that the very structure of modern applications access makes this essential.

Virtually all applications now are delivered over the top, no matter who owns the assets. If you want proof, think about 5G. It now is the second mobile network where the standards were--and are--all about connecting computing devices. Voice support was an overlay for 4G, and so far is not even part of the discussion for 5G.

Think about that. A service that includes, as a core function, the ability to talk and text has, for the last two generations, treated voice as an afterthought. There is a very good reason. Voice--no matter who provides it--now is an OTT application, just like any other.

In other words, OTT is not a choice, it is a basic reality of the way value is delivered in the new communications ecosystem.

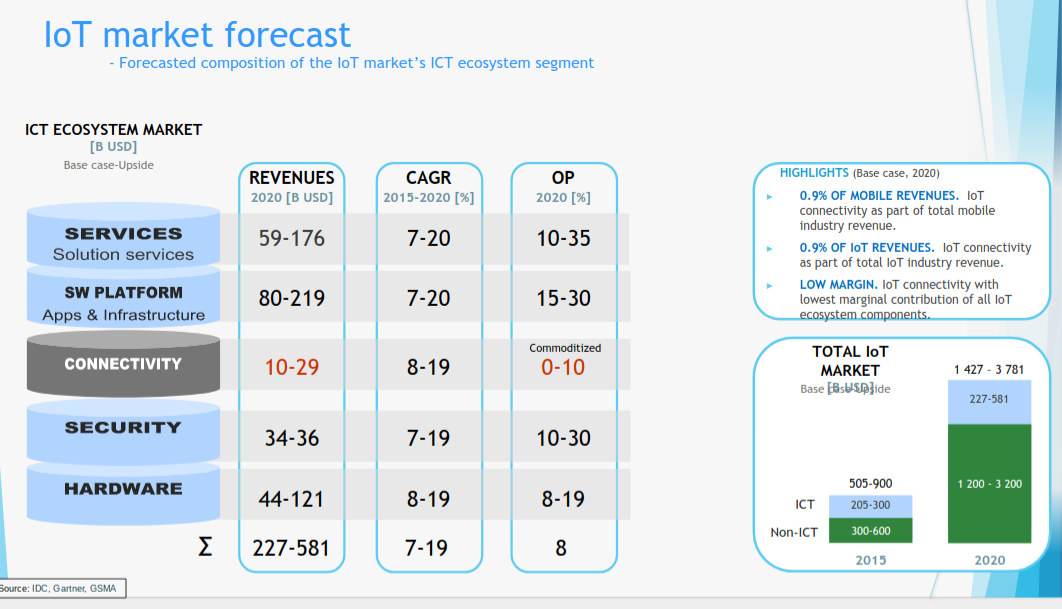

That is likely to be the case for internet of things as well. Value will be supplied in all sorts of ways. But the largest amounts of value, quantified as revenue, will happen in the services layer and the platform layer (all the OTT apps), according to John Kjellemo of Yandex.

Others might put the app layer at the top and the platform layer right below, but the net impact is the same. As much as 65 percent of total ecosystem revenue might accrue to the IoT apps enterprises and people want to use, or the platforms and integration services that support such use.

In what is a sobering forecast, Yandex, looking at available forecasts, believes it is possible that in 2020 less than one percent of mobile service provider total revenue will be generated by connectivity revenues, and a similar “less than one percent” of total IoT ecosystem revenue will be contributed by connectivity services.

In other words, even if 5G proves a resoundingly big deal for internet of things revenue, it still might be almost insignificant as a driver of mobile operator revenue, and will have relatively low profit margins as well.

Source: Yandex

No comments:

Post a Comment