Lots of investors operate on the premise that spectrum has value, even if the owner doesn't really want to be in the service provider business. In fact, some would argue, with good reason, that entrepreneurs such as Craig McCaw always have operated on the theory that it always is good to acquire spectrum, as it is good to acquire land, irrespective of the immediate ability to build an operating business using such spectrum.

If fact, much spectrum originally licensed to support non-profit educational purposes (Multichannel Multipoint Distribution Service, for example) has been redeployed to support mobile communications. Leading U.S. cable operators also have invested in mobile spectrum ownership over the past couple of decades, eventually selling that spectrum rather than building operating businesses.

For that reason, many observers have insisted that Dish Network's actual objective is to sell its now more-valuable spectrum to another service provider, rather than building and operating its own mobile network.

According to that view, Dish Network will do enough to deploy an AWS-4 network, at minimum cost, to meet the FCC’s construction criteria, to persuade a potential buyer such as AT&T to purchase either Dish Network in total or at least the 4G spectrum assets.

Others argue that Dish really is serious about getting into the high-speed access business, and therefore does need to create a 4G network.

Still, there has been an argument argument for decades that, sooner or later, both Dish Network and DirecTV would be acquired by AT&T and Verizon, both to bolster video entertainment business market share.

If so, then the mobile spectrum would simply be added value for the buyer.

Friday, December 21, 2012

What Does Dish Actually Want from LTE?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Will UK 4G Auction Change Market Structure?

There often is hope that major spectrum auctions will increase the amount of competition in a market, sometimes by enticing and enabling new entrants to enter a market. Regulators often specify that some blocks of spectrum are reserved for such new entrants, for example.

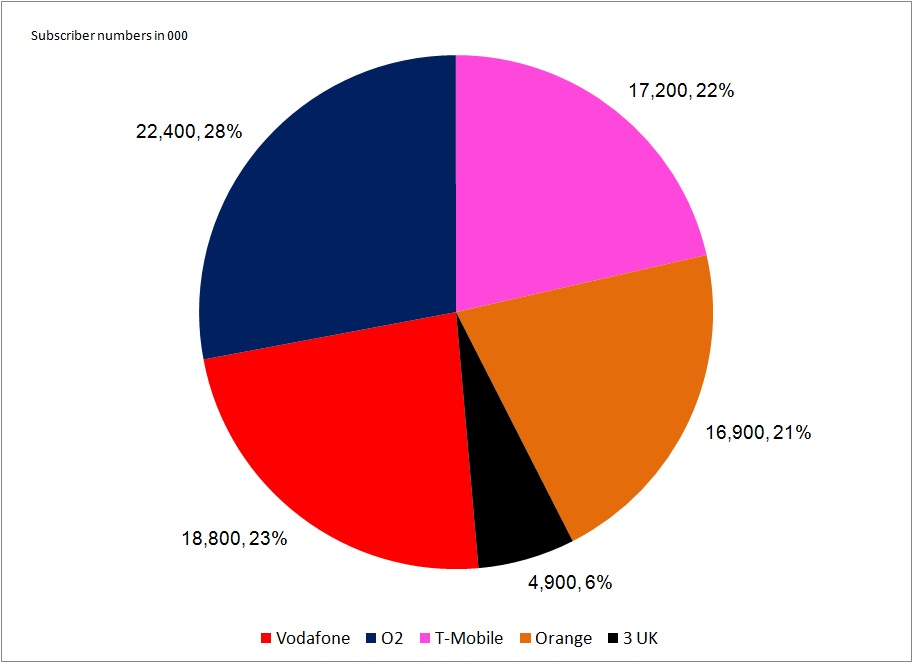

The upcoming U.K. 4G spectrum auctions are likely to see "new" bidders, but the actual amount of impact on the mobile market is likely to be rather insignificant, some would argue. Already, three new names have surfaced as bidders, including BT, which has been barred from the mobile business by regulator action.

Everything Everywhere; HKT Company, a subsidiary of Hong Kong operator PCCW; Three owner Hutchison 3G; MLL Telecom; Niche Spectrum Ventures (BT Group); O2's parent firm Telefónica UK and Vodafone are the seven bidders that have paid the entry fee for the auction.

That naturally raises speculation about whether BT might try and get back into the mobile business as a facilities-based provider, where it today operates as a virtual mobile network operator.

That appears to be unlikely, as BT is probably more interested in using spectrum to reach households it cannot get to using its fixed network.

So some might argue the auctions have little chance of upsetting the current market structure in the United Kingdom. Wireless Intelligence predicts that, by 2014, the same four leaders of the 3G market also will top the 4G market.

The upcoming U.K. 4G spectrum auctions are likely to see "new" bidders, but the actual amount of impact on the mobile market is likely to be rather insignificant, some would argue. Already, three new names have surfaced as bidders, including BT, which has been barred from the mobile business by regulator action.

Everything Everywhere; HKT Company, a subsidiary of Hong Kong operator PCCW; Three owner Hutchison 3G; MLL Telecom; Niche Spectrum Ventures (BT Group); O2's parent firm Telefónica UK and Vodafone are the seven bidders that have paid the entry fee for the auction.

That naturally raises speculation about whether BT might try and get back into the mobile business as a facilities-based provider, where it today operates as a virtual mobile network operator.

That appears to be unlikely, as BT is probably more interested in using spectrum to reach households it cannot get to using its fixed network.

So some might argue the auctions have little chance of upsetting the current market structure in the United Kingdom. Wireless Intelligence predicts that, by 2014, the same four leaders of the 3G market also will top the 4G market.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, December 20, 2012

Is Advertising a Violation of Network Neutrality?

Is advertising a violation of network neutrality? It's a rhetorical question, since advertising is not, as such, a network neutrality issue.

But there are applications of advertising, in an Internet access context, that can appear to be such violations.

Some object, for example, to ISPs making deals with advertisers or content companies regarding use of bandwidth to show movie trailers or other content.

Some object, for example, to ISPs making deals with advertisers or content companies regarding use of bandwidth to show movie trailers or other content.

In other words, some service provider executives think it is reasonable to allow third party advertisers to "sponsor" use of bandwidth, as advertisers now sponsor and help defray the cost of content consumption by end users.

Service providers use the analogy of "toll free" calling, where the cost of network use or a session is paid for by a third party, not the end user. In principle, two-sided business models, where a service or application provider earns revenue both from subscribers and business partners is an essential part of many content and media business models.

And advertising is why most users do not pay direct fees to use Google search, Facebook, Twitter or other popular Internet apps and sites.

That is not to say any such retail charging mechanisms would be easy to implement, or easy for users to understand or embrace. It might be easier to create plans that provide clear incentives to use video only on Wi-Fi networks, such as offering "no-video" plans that are cheaper than other plans that are unrestricted.

Where such proposals are tricky is when they raise the issue of predatory activity on the part of access providers. But it is tricky. On any IP network, it is possible to provide both "Internet access" and "managed services" such as carrier voice or entertainment video and messaging.

Those tricky issues aside, advertising, sponsorship or other forms of third party revenue are not violations of network neutrality, which has to do with issues such as blocking of applications or other potential gate keeping functions.

Advertising, sponsorship and other third party revenue sources are just that, revenue sources. Over time, ISPs contending with ever-higher bandwidth consumption related specifically to video might be compelled to turn to third party sources of revenue, as there are limits to how much consumers will pay for some apps and services.

But there are applications of advertising, in an Internet access context, that can appear to be such violations.

Some object, for example, to ISPs making deals with advertisers or content companies regarding use of bandwidth to show movie trailers or other content.

Some object, for example, to ISPs making deals with advertisers or content companies regarding use of bandwidth to show movie trailers or other content. In other words, some service provider executives think it is reasonable to allow third party advertisers to "sponsor" use of bandwidth, as advertisers now sponsor and help defray the cost of content consumption by end users.

Service providers use the analogy of "toll free" calling, where the cost of network use or a session is paid for by a third party, not the end user. In principle, two-sided business models, where a service or application provider earns revenue both from subscribers and business partners is an essential part of many content and media business models.

And advertising is why most users do not pay direct fees to use Google search, Facebook, Twitter or other popular Internet apps and sites.

That is not to say any such retail charging mechanisms would be easy to implement, or easy for users to understand or embrace. It might be easier to create plans that provide clear incentives to use video only on Wi-Fi networks, such as offering "no-video" plans that are cheaper than other plans that are unrestricted.

Where such proposals are tricky is when they raise the issue of predatory activity on the part of access providers. But it is tricky. On any IP network, it is possible to provide both "Internet access" and "managed services" such as carrier voice or entertainment video and messaging.

Those tricky issues aside, advertising, sponsorship or other forms of third party revenue are not violations of network neutrality, which has to do with issues such as blocking of applications or other potential gate keeping functions.

Advertising, sponsorship and other third party revenue sources are just that, revenue sources. Over time, ISPs contending with ever-higher bandwidth consumption related specifically to video might be compelled to turn to third party sources of revenue, as there are limits to how much consumers will pay for some apps and services.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

"Voice" Increasingly is Synonymous with "Mobile"

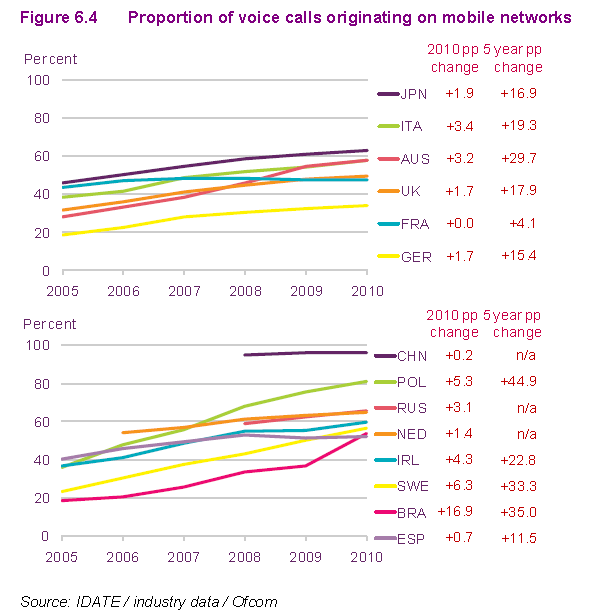

There’s a relatively simple reason people globally prefer to use mobile for voice. In many markets, mobile is the only way to make a call. In 2010, about 90 percent of total call volumes in Brazil, Russia and China occurred on a mobile device.

There’s a relatively simple reason people globally prefer to use mobile for voice. In many markets, mobile is the only way to make a call. In 2010, about 90 percent of total call volumes in Brazil, Russia and China occurred on a mobile device.

In other markets where both mobile voice and fixed voice are available, mobile is cheaper than using fixed services. In these markets, retail pricing and packaging, not just user preferences, drive usage. In addition to convenience, where mobile calling is cheaper than fixed calling, there is less incentive to use the fixed network.

On the other hand, where fixed network calling is quite cheap, users tend to use the fixed network more.

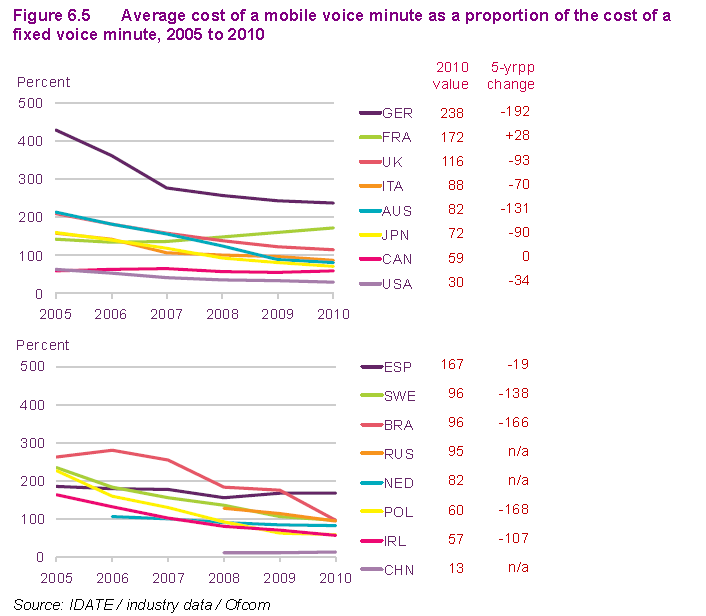

France and Spain were the only countries where the mobile premium, compared to fixed network calling, increased in 2010. In France, the cost of mobile calls relative to fixed voice calls has been increasing since 2006, while in Spain this has been true since 2008, Ofcom, the U.K. communications regulator, says.

France and Spain were the only countries where the mobile premium, compared to fixed network calling, increased in 2010. In France, the cost of mobile calls relative to fixed voice calls has been increasing since 2006, while in Spain this has been true since 2008, Ofcom, the U.K. communications regulator, says. In both countries the average cost of mobile calls also has been falling, meaning that the increase in the mobile premium is a result of the rate of decline in fixed prices being greater than that of mobile calls.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wednesday, December 19, 2012

Can Carriers Afford "Unlimited" Internet Access?

With the caveat that retail price is not necessarily directly related to cost, it sometimes might be possible for an Internet service provider to offer truly limitless Internet access, for a while. That tends to happen only when a brand-new network, operated by an upstart trying to take share, first comes to market.

Under those conditions, the network has plenty of capacity, and it is customers that are in short supply. Assuming that service provider actually is able to make a business of Internet access, the number of customers soon will force a change in such policies at some point, to encourage customers to make choices about how much they use.

Also with the caveat that some think there really is not a bandwidth issue faced by major ISPs, Internet access actually is more akin to many other network services, and unlike a few that charge the equivalent of "flat rates."

The classic example of a "flat rate" network service is cable TV, which allows users "unlimited" use of all the channels, on multiple sets or devices, for the same charge. But that is a multicast service, which has important bandwidth implications.

Essentially a multicast service sends one copy, usable by all users, on a point to multipoint basis. Satellite TV, broadcast TV and broadcast radio work the same way. Metering doesn't matter, because there are zero bandwidth implications for usage, high or low.

No more bandwidth actually is consumed no matter how many customers decide to watch at once, or how many customer devices are in use at any one time.

Internet access is a point-to-point medium, like a voice call, a videoconference, water, waste water or electrical service. There, each unit of additional usage really does have network implications.

At least in part, that is why unlimited Internet access is disappearing. On networks with high usage, there are "peak" hour and "peak day" dimensions to usage. And though it often seems "unfair" to some observers that usage is metered at some level even when the networks are lightly used, that isn't the point.

Every communications network (point to point) has to be sized for "peak" usage, not "average" usage.

So ISPs will have to shift to some form of metered usage over time, even if only to encourage people to use the network at off peak hours, rather than peak hours. Mobile ISPs have been bigger problems, as some parts of their networks have very-high usage on a sustained basis, while other parts are more lightly used.

Any cell site right beside a major highway will become congested during rush hour. Some suburban cells might not become seriously congested at any hour of the day. Some downtown urban sites with high foot traffic might be heavily used during working hours, but lightly used during non-work hours, and on weekends.

The whole point of metering is that metering also allows service providers to create incentives for using the network at times when capacity is not a problem. That's the whole theory behind weekend and evening calling rates, which were important in the past.

The other problem is video, which has bandwidth implications an order of magnitude or two orders of magnitude greater than voice, for example. While nobody seems to think retail rates actually can rise by an order of magnitude or two orders of magnitude, even if usage does grow that much, the additional usage carries real costs, and those costs have to be recovered.

So can a typical ISP, with a serious number of customers, actually afford to offer truly unlimited access, if those customers start watching Internet-delivered video? Probably not. An order of magnitude worth of network is an expensive thing.

One might hope more-efficient suppliers might enter any local market, but any large ISP will over time, experience higher costs "per unit," even if that supplier originally started out as a low-cost supplier.

We can quibble about the cost elements, but those elements will develop, over time, especially in highly-competitive markets such as Internet access.

Under those conditions, the network has plenty of capacity, and it is customers that are in short supply. Assuming that service provider actually is able to make a business of Internet access, the number of customers soon will force a change in such policies at some point, to encourage customers to make choices about how much they use.

Also with the caveat that some think there really is not a bandwidth issue faced by major ISPs, Internet access actually is more akin to many other network services, and unlike a few that charge the equivalent of "flat rates."

The classic example of a "flat rate" network service is cable TV, which allows users "unlimited" use of all the channels, on multiple sets or devices, for the same charge. But that is a multicast service, which has important bandwidth implications.

Essentially a multicast service sends one copy, usable by all users, on a point to multipoint basis. Satellite TV, broadcast TV and broadcast radio work the same way. Metering doesn't matter, because there are zero bandwidth implications for usage, high or low.

No more bandwidth actually is consumed no matter how many customers decide to watch at once, or how many customer devices are in use at any one time.

Internet access is a point-to-point medium, like a voice call, a videoconference, water, waste water or electrical service. There, each unit of additional usage really does have network implications.

At least in part, that is why unlimited Internet access is disappearing. On networks with high usage, there are "peak" hour and "peak day" dimensions to usage. And though it often seems "unfair" to some observers that usage is metered at some level even when the networks are lightly used, that isn't the point.

Every communications network (point to point) has to be sized for "peak" usage, not "average" usage.

So ISPs will have to shift to some form of metered usage over time, even if only to encourage people to use the network at off peak hours, rather than peak hours. Mobile ISPs have been bigger problems, as some parts of their networks have very-high usage on a sustained basis, while other parts are more lightly used.

Any cell site right beside a major highway will become congested during rush hour. Some suburban cells might not become seriously congested at any hour of the day. Some downtown urban sites with high foot traffic might be heavily used during working hours, but lightly used during non-work hours, and on weekends.

The whole point of metering is that metering also allows service providers to create incentives for using the network at times when capacity is not a problem. That's the whole theory behind weekend and evening calling rates, which were important in the past.

The other problem is video, which has bandwidth implications an order of magnitude or two orders of magnitude greater than voice, for example. While nobody seems to think retail rates actually can rise by an order of magnitude or two orders of magnitude, even if usage does grow that much, the additional usage carries real costs, and those costs have to be recovered.

So can a typical ISP, with a serious number of customers, actually afford to offer truly unlimited access, if those customers start watching Internet-delivered video? Probably not. An order of magnitude worth of network is an expensive thing.

One might hope more-efficient suppliers might enter any local market, but any large ISP will over time, experience higher costs "per unit," even if that supplier originally started out as a low-cost supplier.

We can quibble about the cost elements, but those elements will develop, over time, especially in highly-competitive markets such as Internet access.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

People Access the Internet Everywhere, All the Time

A survey of abourt 60,000 U.S. users simply confirms what you would assume, namely that people now use their smart phones to use the Internet virtually everywhere, Forrester Research reports.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobile Data Plans Will Grow 10 Times Bigger by 2015

Real-time entertainment applications on mobile devices (smartphone and tablets) being used on fixed access networks accounted for nine percent of all traffic in North America, according to Sandvine.

By 2015, Sandvine believes mobile devices will account for 20 percent of all traffic on North American fixed access networks.

By 2015, Sandvine believes mobile devices will account for 20 percent of all traffic on North American fixed access networks.

In the past three years on North American fixed access networks, real-time entertainment has almost doubled its share of traffic, now accounting for 58.6 percent of all peak period traffic, Sandvine says.

Sandvine expects real-time entertainment will account for over two thirds of peak period traffic by 2015.

For those reasons, Sandvine predicts mobile users will demand service packages with ten times the monthly quota that is available in 2012. The clear business problem for mobile ISPs is that virtually nobody believes service providers can charge an order of magnitude more for mobile broadband.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Costs of Creating Machine Learning Models is Up Sharply

With the caveat that we must be careful about making linear extrapolations into the future, training costs of state-of-the-art AI models hav...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...